The Best Strategy To Use For Home Renovation Loan

The Best Strategy To Use For Home Renovation Loan

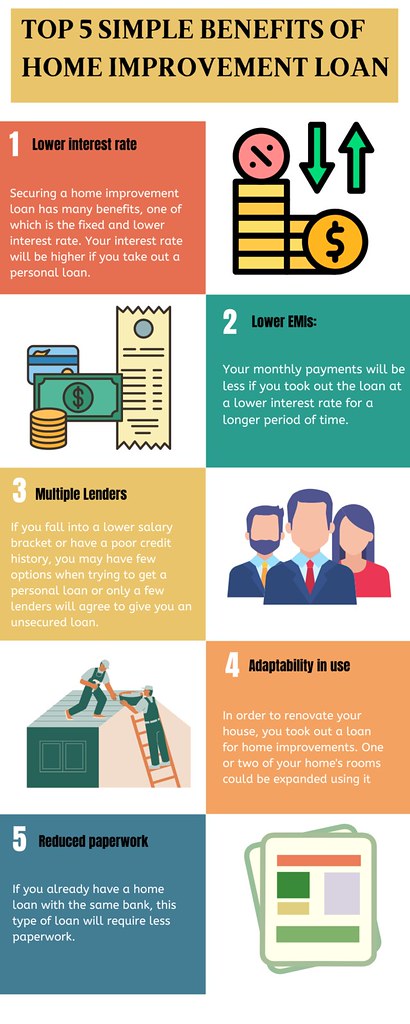

Blog Article

Unknown Facts About Home Renovation Loan

Table of ContentsLittle Known Facts About Home Renovation Loan.Excitement About Home Renovation LoanExcitement About Home Renovation LoanThe smart Trick of Home Renovation Loan That Nobody is DiscussingThe Ultimate Guide To Home Renovation Loan

Take into consideration a house restoration lending if you want to renovate your house and give it a fresh look. With the help of these loans, you might make your home extra aesthetically pleasing and comfy to live in.There are plenty of financing alternatives available to assist with your home remodelling. The appropriate one for you will rely on just how much you need to borrow and how rapidly you wish to pay it off. Brent Differ, Branch Supervisor at Assiniboine Lending institution, offers some functional suggestions. "The first thing you ought to do is obtain quotes from several contractors, so you understand the fair market price of the job you're obtaining done.

The main benefits of using a HELOC for a home restoration is the versatility and reduced rates (commonly 1% over the prime rate). Furthermore, you will just pay passion on the amount you withdraw, making this a great option if you require to pay for your home improvements in stages.

The major drawback of a HELOC is that there is no set payment timetable. You need to pay a minimum of the passion each month and this will certainly increase if prime prices increase." This is an excellent financing alternative for home remodellings if you wish to make smaller sized month-to-month repayments.

What Does Home Renovation Loan Do?

Offered the possibly long amortization period, you might finish up paying significantly more passion with a mortgage refinance contrasted with various other financing alternatives, and the expenses connected with a HELOC will additionally apply. home renovation loan. A home loan refinance is properly a new home mortgage, and the rates of interest can be greater than your existing one

Prices and set up expenses are normally the like would spend for a HELOC and you can settle the financing early without any penalty. A few of our consumers will begin their improvements with a HELOC and after that switch over to a home equity car loan as soon as all the prices are confirmed." This can be an excellent home remodelling funding alternative for medium-sized jobs.

Personal car loan prices are commonly greater than with HELOCs usually, prime plus 3%. And they normally have shorter-term periods of 5 years or much less, which suggests greater repayment amounts." With credit score cards, the main drawback is the rates of interest can generally vary between 12% to 20%, so you'll want to pay the balance off promptly.

Home improvement lendings are the funding option that enables homeowners to renovate their homes without having to dip into their financial savings or splurge on high-interest charge card. There are a variety of home renovation financing resources readily available to pick from: Home Equity Credit Line (HELOC) Home Equity Funding Home Mortgage Refinance Personal Lending Charge Card Each of these financing alternatives features unique requirements, like credit history score, owner's income, credit line, and rates of interest.

Our Home Renovation Loan Ideas

Prior to you start of creating your desire home, you possibly desire to understand the a number of types of home restoration fundings available in Canada. Below are a few of one of the most usual kinds of home remodelling lendings each with its own collection of attributes and benefits. It is a type of home renovation financing that permits property owners to borrow an abundant sum of money at a low-interest rate.

These are beneficial for large renovation tasks and have reduced rate of interest than other kinds of personal loans. A HELOC Home Equity Line of Credit scores is comparable to a home equity loan that uses the value of your home as protection. It works as a bank card, where you can borrow according to your needs to money your home restoration tasks.

To be eligible, you should possess either a minimum of a minimum of 20% home equity or if you have a home loan of 35% home equity for a standalone HELOC. Refinancing your home loan process includes replacing your existing home loan with a new one at a lower rate. It reduces your regular monthly settlements and decreases the amount of interest you pay over your lifetime.

Home Renovation Loan - The Facts

For this, you may need to provide a clear building and construction plan and budget for the restoration, including determining the expense for all the materials called for. Additionally, individual financings can be pop over to these guys secured or unsafe with shorter repayment periods (under 60 months) and come with a greater rate of interest, depending on your credit rating and earnings.

Indicators on Home Renovation Loan You Need To Know

Store financing programs, i.e. Store credit score cards are used by numerous home improvement shops in Canada, such as Home Depot or Lowe's. If you're preparing for small home renovation or do it yourself tasks, such as installing brand-new home windows or restroom restoration, obtaining a shop card with important site the seller can be a very easy and quick process.

Report this page